Its native 4K on the biggest AAA title of the generation plus many many more.It's not native 4K on many of the AAA multiplatform games. And when compared to PC settings, X1X is usually running a mix of medium/high settings. I'm sure devs would like to crank up the settings as well.

-

Ever wanted an RSS feed of all your favorite gaming news sites? Go check out our new Gaming Headlines feed! Read more about it here.

-

We have made minor adjustments to how the search bar works on ResetEra. You can read about the changes here.

NPD analyst: "Hardware cycles as we knew them are over"

- Thread starter Atheerios

- Start date

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Yep, can't leave out Sega either. They were well ahead of their time too, so the idea of a hardware refresh being "new" is kinda silly.Or Segas first three consoles and then the fourth using an adaptor.

I'd be day one for a Switch Pro, just give it a way smaller bezel and reasonable boosts to the hardware so that games can comfortably run at 1080p docked. If I was pushing it, I'd also like a revised dock that is capable of upscaling the 1080p image to 4k, but everything about Nintendo tells me that kind of thing is a good five years away for them.Yeah I'm really enjoying this with the Pro, really hope the rumours of a Switch revision in 2019 are true too

Joining the party late with a more powerful system and a great library of games, many of them now discounted, was fantastic, and I'm happy to do that going forward

Unless tech really surprises me in the next couple of years, I'm not sure how big a leap PS5 can even take over it's mid-gen predecessor. 4k60fps would be great but it's only part of the picture when considering what a next gen game ought to look like. Part of me wants them to hold off a few more years. Current gen still looks really impressive to me. And also my PS4 is out for delivery today lol.

And it just arrived! Fuck me I post really slowly when I'm stoned...

To me, it's pretty simple. Xbox is getting a second round of greater revenue from X and PS4 is getting a revenue increase from Pro.

If we look at it from a revenue perspective, then it's pretty easy to see that there will be a big increase in revenue where a lull would expect to be continued.

The other thing though is demand pricing is hitting for both high end and mass market technology shoppers while the value propositions are much better with new game modes and new experiences to share.

It's less that hardware cycles are impermeable or unpredictable as much as today is a world that had never been seen so it wasn't foreseen that the new systems would push this many consoles on the high end.

If we look at it from a revenue perspective, then it's pretty easy to see that there will be a big increase in revenue where a lull would expect to be continued.

The other thing though is demand pricing is hitting for both high end and mass market technology shoppers while the value propositions are much better with new game modes and new experiences to share.

It's less that hardware cycles are impermeable or unpredictable as much as today is a world that had never been seen so it wasn't foreseen that the new systems would push this many consoles on the high end.

This is actually a really good point. It looks gorgeous, I hear it's relatively quiet, the modular internals are a self-repairers dream and it plays UHD Blu Ray. There's definitely more to it that just power.

It's basically silent even when playing red dead 2 or odyssey. It's a dream.

We should be happy since console gaming was supposed to die in 2012 remember?

I think a lot of families and budget gamers are finally buying it at this point in the cycle. Xbox and Sony should get permanent $199 skus out in 2019 to squeeze even more life out of these systems.

I think November 2020 will see both console makers launch new systems.

I think a lot of families and budget gamers are finally buying it at this point in the cycle. Xbox and Sony should get permanent $199 skus out in 2019 to squeeze even more life out of these systems.

I think November 2020 will see both console makers launch new systems.

Honestly mobile has really helped out the switch too. Devs are willing to Target switch as the install base is there for both switch and higher end Android/iOS gpus. Basically gens are done because devs are willing to Target lots of different power levels/gpus, much like in the PC space, because it increases their revenue potential.

I think we will see base ps4 and Xbox one (and switch) ports for a long ass time from most 3rd parties.

Sure there will still be tech showcases but those will mainly be platform exclusives designed as system sellers. You'll see less and less 3rd parties pushing the envelope graphically, at least if they can't easily scale it down/port it to weaker hardware.

I think we will see base ps4 and Xbox one (and switch) ports for a long ass time from most 3rd parties.

Sure there will still be tech showcases but those will mainly be platform exclusives designed as system sellers. You'll see less and less 3rd parties pushing the envelope graphically, at least if they can't easily scale it down/port it to weaker hardware.

Why will there be another mid gen reresh? This time around it was necessary for 4K tvs, and this upgrade brought about a much cleaner IQ. What would be the point of another mid gen fresh? The cleaner IQ made the graphics look much better, this reresh had very obvious advantage over the base console. Next time around there may not be any obvious reason to have a refresh.

Because it sells hardware.

You could do nothing but make the console smaller and give it a sleeker, classier case and half the users will upgrade.

Why will there be another mid gen reresh? This time around it was necessary for 4K tvs, and this upgrade brought about a much cleaner IQ. What would be the point of another mid gen fresh? The cleaner IQ made the graphics look much better, this reresh had very obvious advantage over the base console. Next time around there may not be any obvious reason to have a refresh.

Yeah, not sure if there will be the need for a mid-gen refresh next time. The 4K TV explosion was the reason for PS4 Pro. And hardware improvements are slowing down more and more every year. End of Moore's Law and all. What will be the point of a PS5 Pro two years later? A couple more fps here and there?

Yeah I think all of those PS5 speculation threads and folks hyped for a PS5 with no known games yet are crazy.

The current gen is great and only getting better. Why would we need new hardware yet? I could wait til 2021 even.

The current gen is great and only getting better. Why would we need new hardware yet? I could wait til 2021 even.

This has been evident to anybody paying close attention.

A lot of the rhetoric around consoles is based on years, even decades ago situations and strategies.

In reality it's all uncharted territory from here.

I'm still team 2021 before we get any new hardware from either Sony or Microsoft.

Makes Zero sense for new consoles to drop before then.

A lot of the rhetoric around consoles is based on years, even decades ago situations and strategies.

In reality it's all uncharted territory from here.

I'm still team 2021 before we get any new hardware from either Sony or Microsoft.

Makes Zero sense for new consoles to drop before then.

Not only the 360, FY 2012 was also PS3 best year (same age).Yeah. Was about to post that wasn't his true to some degree also last gen. 360 had its peak year in 2011. It was older than PS4/XBO are at the moment.

I just don't see it with rumblings of the next hardware cycle getting louder right now. Sure, the PS5/XS/SW2 cycle will probably be different in some ways, but there have always been "anomalies" like PS2, Wii and PS4, which shape a generation differently than more "normal" consoles. I think that in the end, we'll get what can be called a pretty normal hardware cycle, in that there will be at least one "anomaly" and some things will be different than in previous gens, but right now it looks more like a traditional next gen hardware cycle than it did just a couple of years ago.

Yeah, not sure if there will be the need for a mid-gen refresh next time. The 4K TV explosion was the reason for PS4 Pro. And hardware improvements are slowing down more and more every year. End of Moore's Law and all. What will be the point of a PS5 Pro two years later? A couple more fps here and there?

Yeah I'm sure PS5 games will look amazing, but PS4 games on the Pro already look amazing

Then again I remember a lot of people saying PS4 games looked like PS3 games back in 2013/14 on GAF, so what do we know

Console devs are becoming comfortable with the PC model of targeting hardware below and above the actual hardware you're on. Sony and MS also not interested in resetting their customer base with each console anymore. I think you're going to start seeing multi-generation discs become common.

It was the right move from Sony and MS. Remember all the doomsayers saying it would kill base versions and such? Instead mid-gen refreshes revitalized the market and made this gen not feel stale at all.

If we go to 2020 before new consoles show up that's just fine considering how many great games are being released.

However I bet Xbone X and Pro will get dropped come PS5 and Xbox Duo days to keep base versions for price sensitive markets.

If we go to 2020 before new consoles show up that's just fine considering how many great games are being released.

However I bet Xbone X and Pro will get dropped come PS5 and Xbox Duo days to keep base versions for price sensitive markets.

Is it? I don't see what's compelling about getting a new console after 2-3 years unless you have that much disposable income. PS4 Pro is really targeted towards people looking to get a more powerful console and not really upgrading from one. That and it complements their lineup of 4K products.I got the opposite impression. Pretty sure both hardware upgrades are popular. Also pretty sure plenty of people upgraded their consoles.

This is a weird position; most developers have been doing this for decades, including different feature levels within generations, different feature levels across generations, and then PC targets with dynamic configuration sitting on the side of both of them. I've done all of these in my twenty years in the industry.Console devs are becoming comfortable with the PC model of targeting hardware below and above the actual hardware you're on.

I'm 40, so I've seen every generation from 2 on, and I can assure you diminishing returns play into it. The jump in capabilities has been less and less obvious in recent cycles. Aside from core gamers who want that power boost, the only incentive for people to upgrade is to be able to play games they can't get on their current console.

Is it? I don't see what's compelling about getting a new console after 2-3 years unless you have that much disposable income. PS4 Pro is really targeted towards people looking to get a more powerful console and not really upgrading from one. That and it complements their lineup of 4K products.

First I'll say that, they're most likely not selling better than the original PS4 or Xbox. However, many people including myself like the power. There's many on here that upgraded their consoles and I know people who just upgraded as well. We live in a world where people spend an outrageous amount of eating out, maintaining social lives and other forms of hobbies. Trading in a console for a new one for a few hundred dollars isn't a burden. Especially when you see the amount of people dropping 900 plus dollars a year on phones or upgrading contracts for those phones. It's a consumer culture that's for sure. I think there's enough of a consumer group that's wants these things that they will. Those companies and have the data so we will see what they do with next gen if a mid refresh is even a thing unless streaming tech disrupts it. I agree that 4K could have drove those sales, so without that next gen, maybe we won't see the need there. I think the big concern right now is losing people to PC. Where there are people willing to pay more for better experiences. I think that pool of people is small in comparison to the ppl who just want a powered up console who is probably still smaller than the regular console buyers. But I bet it's still a big enough market. Wish someone had some numbers to show how many people upgraded. I know that Sony and Microsift know.

It makes far more sense to do cross gen games for the first year to year and a half than it does to just drop the mid-gen bumps, especially when that's the timeframe we traditionally see cross generation titles anyway.

It makes far more sense to do cross gen games for the first year to year and a half than it does to just drop the mid-gen bumps, especially when that's the timeframe we traditionally see cross generation titles anyway.

Exclusive titles sell consoles.

Who's going to buy a next gen machine when the current gen console plays the same games?

That's why Nintendo releases a new Mario Kart every gen. That's why Uncharted 4 didn't get a PS3 version

Exclusive titles sell consoles.

Who's going to buy a next gen machine when the current gen console plays the same games?

That's why Nintendo releases a new Mario Kart every gen. That's why Uncharted 4 didn't get a PS3 version

Worst example ever. Have you even heard of Mario Kart 8?

The Wii U is an exception cos no one bought one

Same.I'm 40, so I've seen every generation from 2 on, and I can assure you diminishing returns play into it. The jump in capabilities has been less and less obvious in recent cycles. Aside from core gamers who want that power boost, the only incentive for people to upgrade is to be able to play games they can't get on their current console.

I started gaming on the 2600. So we've seen some things, lol.

I can't remember when most powerful ever played a part in my buying decision. As much as I don't really like Nintendo right now, I've gotten every home console they made...because of exclusives.

Controller, exclusives, friends, co workers played a waaaay bigger part.

.....And the counter to this always is.....

Imagine how less the Wii U would have sold if not for exclusives. If they were depending on folks with a Wii U to buy 3rd party games it would have sold alot worse.

Exactly.

Exclusive titles sell consoles.

Who's going to buy a next gen machine when the current gen console plays the same games?

That's why Nintendo releases a new Mario Kart every gen. That's why Uncharted 4 didn't get a PS3 version

Mario Kart 8 and BotW are on the Wii U and people bought the Switch for it. Bad example.

Maybe people will buy a good console with a clear message (i.e. The Switch) for exclusives, but not a bad console with an unclear purpose (i.e. the Wii U)?

I probably would have bought a WiiU for BotW if it had been exclusive, but God damn I would have resented having to do so. On the other hand, the Switch is the first console I have ever bought within 12 months of launch (mainly to just get on that BotW hype train), zero regrets.

I probably would have bought a WiiU for BotW if it had been exclusive, but God damn I would have resented having to do so. On the other hand, the Switch is the first console I have ever bought within 12 months of launch (mainly to just get on that BotW hype train), zero regrets.

Mario Kart 8 and BotW are on the Wii U and people bought the Switch for it. Bad example.

NOBODY BOUGHT A WII U the existence of Wii U ports is the anonomaly and it doesn't negate 30 years of 'exclusives sell consoles'... christ

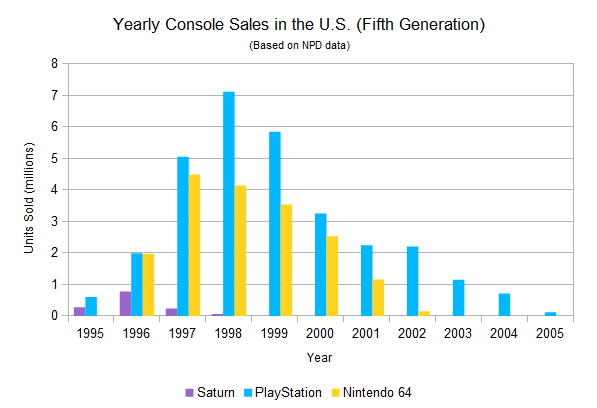

Do we have any updated graphs for tracking console sales? Especially across different gens.

I remember we used to have people posting them all the time but never see them anymore.

I remember we used to have people posting them all the time but never see them anymore.

If the PS5 does 4K 60 , What does the PS5 pro gonna do? FAKE 8K 30?

Raytracing?

Exactly.Maybe people will buy a good console with a clear message (i.e. The Switch) for exclusives, but not a bad console with an unclear purpose (i.e. the Wii U)?

I probably would have bought a WiiU for BotW if it had been exclusive, but God damn I would have resented having to do so. On the other hand, the Switch is the first console I have ever bought within 12 months of launch (mainly to just get on that BotW hype train), zero regrets.

Like I never got a chance to play 3D World, and I hope a Switch port gets made.

I'll be damn if get a Wii U again just for 3D World. My Wii U was stolen in a robbery.

Seamus Blackley had a real interesting take on this on Twitter...

This has been what I have always been saying

The difference in graphics is no longer a huge leap . We are slowly hitting that ceiling. If I am interpreting what he tweeted right.

Next gen consoles just for a small increase in graphical detail ? No thanks

To be fair that's exactly how this gen launched.Next gen consoles just for a small increase in graphical detail ?

Anyway VR is the tech differentiator Blackley doesn't notice. Its far more drastic than anything we do with graphics on flat panels, and even raytracing won't really come into its own until we have it in VR. Its not going mainstream for a good while longer either though.

I think this remains to be seen. 4k hook was convenient this time, if it becomes pc like 'oh its x% faster' I really question adoption rates being this good.Seamus Blackley had a real interesting take on this on Twitter...

Not sure if serious. Did you forget The Order: 1886, Until Dawn, Assassin's Creed Unity, Infamous: Second Son were all out in that first year? Unity is still probably the best looking Assassin's Creed to me. The other locales are more eye popping across deserts of Egypt and islands of Greece, but what they were doing with the crowds on screen was insane.

There are two reasons why I think this is happening:

- The typical console gamer in a traditional sense is now a full fledged adult. This means they have the disposable income to purchase upgrades and rival consoles. The PS4 Pro/Xbox One X have done very well, while 70% of Switch owners have another gaming console. Maybe I'm just out of touch,but I believe this is a major reason why the "console wars" is so relatively cool compared to previous generations. Because most gamers don't have to get jealous of another console if it has games they want, they'll just simply buy it instead because they are now adults with money.

- There are very few games that need the latest and greatest power. Consider this, the Nintendo Switch can run most PS4 games satisfactory. Now yes, the Switch wouldn't be able to handle say Marvel's Spiderman, but anything from Undertale to Wolfenstein II: TNC the system can handle, respectfully so I might add. Much of the biggest titles in gaming right now (e.g. Fortnite and League of Legends) can run on pretty much anything. Choosing what device to play these games on is often a question of resolution vs portability. Therefore, a lot of people aren't too worried even if a PS5 or Xbox TWO comes out in the not so distant future, because they know they will be satisfied with their new console purchase and know it will be supported.

- The typical console gamer in a traditional sense is now a full fledged adult. This means they have the disposable income to purchase upgrades and rival consoles. The PS4 Pro/Xbox One X have done very well, while 70% of Switch owners have another gaming console. Maybe I'm just out of touch,but I believe this is a major reason why the "console wars" is so relatively cool compared to previous generations. Because most gamers don't have to get jealous of another console if it has games they want, they'll just simply buy it instead because they are now adults with money.

- There are very few games that need the latest and greatest power. Consider this, the Nintendo Switch can run most PS4 games satisfactory. Now yes, the Switch wouldn't be able to handle say Marvel's Spiderman, but anything from Undertale to Wolfenstein II: TNC the system can handle, respectfully so I might add. Much of the biggest titles in gaming right now (e.g. Fortnite and League of Legends) can run on pretty much anything. Choosing what device to play these games on is often a question of resolution vs portability. Therefore, a lot of people aren't too worried even if a PS5 or Xbox TWO comes out in the not so distant future, because they know they will be satisfied with their new console purchase and know it will be supported.

You don't have to not have exclusives under my scenario. Uncharted 5 releases on PS5 only, while MLB The Show hits the PS5 and PS4Pro. Halo 7 hits Xbox 4, Halo Wars 3 hits the X1X and Xbox 4.Exclusive titles sell consoles.

Who's going to buy a next gen machine when the current gen console plays the same games?

That's why Nintendo releases a new Mario Kart every gen. That's why Uncharted 4 didn't get a PS3 version

Multiplats work off of one disc and scale resolution, textures, and whatnot based on the hardware they're in, just like with the current systems and PC games, only without as much console user tinkering.

The two ideas aren't mutually exclusive.

I'm a little late to this discussion. I was referred to it the other day but I haven't gotten around to replying because of lack of time. Apologies if it's considered gauche here at ERA to bump a thread that's been inactive for a week.

The changes in sales curves this generation are entirely explicable as being the result of the same forces that influence the sales curves of every other system. The timing and degree of price cuts, the effects of new models (be they form factor changes or full spec upgrades), and the effects of major system-selling software. Systems used to have a clear growth-peak-decline pattern, but as Mr. Piscatella points out that's no longer the case.

It used to be that systems would have a pronounced peak in sales somewhere in their first three years on the market.

Last generation, we saw greatly delayed peaks, with the 360 and PS3 peaking in 2011, their sixth and fifth full years, respectively. The Wii had a fairly normal curve for a Nintendo system, peaking in its second full year, but for conventional consoles we ended up with a protracted generation.

Why did this happen? Well, I think the best explanation is because of pricing. Last generation, price cuts for the PS3 & 360 were fewer in number, smaller in terms of percentage drop (and in the 360's case in absolute dollar terms), and spaced out more overall, resulting in systems that declined in price much more slowly and spent most of their lives being more expensive than systems in prior generations.

To keep a long story short, the 360 & PS3 both started off relatively weak and experienced slower growth than the PS2 did, not reaching peak sales until their respective slimline models were issued well into their lifespans. The 360 S produced a significant increase in 360 sales, making 2010 & 2011 a rather pronounced peak period, but a belated one. The PS3 actually exhibited clearer growth, going from very poor prior to its cut to $400, to being able to about match the 360 during the Jan.-Aug. period of 2008, to growing even more once the Slim was released. The PS3's peak was more of a plateau, with 2011 being only slightly higher than 2010 (2009 was only as high as it was thanks to the last four months of that year when the Slim gave its initial boost).

Now, what about the current generation? The PS4 & XBO have spent most of their lives cheaper than the 360 & PS3 in inflation-adjusted terms. As a result, aligned sales have strongly favored the PS4 & XBO (note that the third graph aligns the launches of the PS3 & 360):

But you'll notice that the bulk of the growth, the sharpest increases in the surpluses, have been in the holidays. The PS4 & XBO's combined surplus increased by more than 2.5 million units in the 2016 holiday period alone.

This is because sales have experienced a significant shift towards the holidays this generation thanks to official temporary Black Friday price cuts. While that trend began in 2011, it was solidified this generation. These big Black Friday deals deals have greatly diminished the effects of the permanent price cuts the systems have gotten. It has also resulted in consistently strong holiday sales, with combined PS4+XBO sales in Q4 far exceeding 5 million units for the past three years (and this year may make it a fourth). Compare this to combined PS2+Xbox sales, which only crossed the 5M mark in Q4 once (in 2002), and combined PS3+360 sales, which only did so twice (in 2010 & 2011).

The net effect of this is Gen 8 being more Q4-centric than ever, and total Q1-Q3 sales seeing far less variation than before. The Q1-Q3 period of 2015 saw combined PS4+XBO sales grow less than 3% YoY, while for the same periods in 2016 & 2017 were down about 5% each year. This year has seen Q1-Q3 sales grow something like 17% YoY, which is okay, but is only about 6% higher than Q1-Q3 2015. The biggest variations we've seen are in the holidays, with Q4 2015 being up 30% from Q4 2014 (though that was because Sony didn't offer any big discounts for the PS4 in the 2014 holiday season). Q4 2016 was down nearly 10% YoY, and Q4 2017 nearly matched Q4 2016 (though if you ignore October, the Nov.+Dec. period of 2017 was up about 4% YoY, not a huge difference but it's there).

The siphoning off of Q1-Q3 sales by Q4 (and esp. November) has also resulted in combined PS4+XBO sales in the non-holiday months just barely keeping pace with combined PS3+360 sales. This generation has looked big and healthy for conventional consoles compared to last gen, but you can thank Black Friday for that.

As for this year, the PS4's YoY growth can be attributed entirely to software. God of War, Spider-Man, and Red Dead all moved a good amount of hardware. But ignore April, September, and October, and we see baseline sales that have actually dipped ever so slightly. The Slim & Pro did help out a bit in 2017 (Q1-Q3 sales were up 17-18% YoY), but didn't produce a clear peak, and their upwards effect on sales has clearly ended. 2018 was the Year of the System Seller for the PS4 in the U.S.

As for the XBO, the One X has clearly helped out, with significant YoY improvements this year from a rather mediocre 2017. But again it hasn't produced a clear peak, and Q1-Q3 sales this year were weaker than those in 2015, and roughly flat with 2016. Also, September suggested that the One X effect might be coming to an end, with flat sales YoY for the month (October had Red Dead, which was also a system-seller for the XBO, so we can't make a determination).

The Pro and One X are unlikely to produce further sales growth unless Sony & MS introduce deep price cuts with the intent of having them fully supplant the slimline models. Q1 2019 will be the first big test for PS4 & XBO sales with current models at current prices. If we see both systems down noticeably, then that will likely signal them entering the terminal decline period of their lives. It's possible that deep cuts to the Pro and One X could drive some more sales growth, but with Gen 9 hardware known to be in the works and likely due for release in 2020, it's questionable if the Pro & One X will even get permanent price cuts of any kind. The Pro didn't even get a temporary cut for BF this year. And it's possible that such a cut might not result in any significant growth, as not everyone is likely to upgrade even at a reduced price. Eventually, no amount of attempts to stimulate sales will keep a system's sales from irreversibly declining.

In any case, the effects of the Pro and One X are overstated, and hardware revisions in general haven't had the effects they used to, just like how permanent price cuts haven't had the effects they used to. Without a breakdown between sales of the two, it's difficult to separate the effects of the Slim and Pro for the PS4, but between they two they failed to produce the kind of growth we saw with the PS3 Slim. The XBO S absolutely failed to produce significant growth past its first three months, and while the One X did help make Q1 this year the XBO's best Q1 to date and make Q2 its second-best Q2, it too was nothing like the 360 S in terms of what it did for sales.

Between the shift of a greater portion of annual sales to Q4 thanks to temporary BF price cuts and the relative failure of hardware revisions to produce strong growth, it's no wonder sales curves have been wonky this generation. But nevertheless the console cycle will continue unabated. The PS4 & XBO are at over 48M combined LTD, likely to be north of 53M by year's end. There is a maximum addressable market, with only so many households willing, able, and planning to buy a current-gen console at some point, and eventually Sony & MS will run out of potential customers to sell PS4s & XBOs to. The systems will enter the terminal decline phase of their lives before too long, regardless of their subversion of the usual "growth" and "peak" periods. By the end of 2011, the 360 & PS3 had a combined LTD total of 52.65M units, and in 2012 they began their declines. Since the PS4 & XBO will be at about that point by the end of this year, it wouldn't be a stretch to assume that they're likely going to start declining soon, probably next year, as the number of first-time buyers starts to dwindle. They'll probably end up at about the same ~70M units combined the PS3 & 360 ended up at, maybe slightly higher due to population growth potentially increasing the overall size of the addressable market as well as the potential for more mid-gen upgrades as usual since the Pro & One X were full spec upgrades (the first for home consoles since the Japan-only SuperGrafx) instead of just changes in form factor.

Well, that took longer and went on longer than I wanted, but I wanted to cover all my bases. Sorry if it sounded a bit ramble-y. Hope you all enjoyed the read and my attempts as sales analysis.

The changes in sales curves this generation are entirely explicable as being the result of the same forces that influence the sales curves of every other system. The timing and degree of price cuts, the effects of new models (be they form factor changes or full spec upgrades), and the effects of major system-selling software. Systems used to have a clear growth-peak-decline pattern, but as Mr. Piscatella points out that's no longer the case.

It used to be that systems would have a pronounced peak in sales somewhere in their first three years on the market.

Last generation, we saw greatly delayed peaks, with the 360 and PS3 peaking in 2011, their sixth and fifth full years, respectively. The Wii had a fairly normal curve for a Nintendo system, peaking in its second full year, but for conventional consoles we ended up with a protracted generation.

Why did this happen? Well, I think the best explanation is because of pricing. Last generation, price cuts for the PS3 & 360 were fewer in number, smaller in terms of percentage drop (and in the 360's case in absolute dollar terms), and spaced out more overall, resulting in systems that declined in price much more slowly and spent most of their lives being more expensive than systems in prior generations.

To keep a long story short, the 360 & PS3 both started off relatively weak and experienced slower growth than the PS2 did, not reaching peak sales until their respective slimline models were issued well into their lifespans. The 360 S produced a significant increase in 360 sales, making 2010 & 2011 a rather pronounced peak period, but a belated one. The PS3 actually exhibited clearer growth, going from very poor prior to its cut to $400, to being able to about match the 360 during the Jan.-Aug. period of 2008, to growing even more once the Slim was released. The PS3's peak was more of a plateau, with 2011 being only slightly higher than 2010 (2009 was only as high as it was thanks to the last four months of that year when the Slim gave its initial boost).

Now, what about the current generation? The PS4 & XBO have spent most of their lives cheaper than the 360 & PS3 in inflation-adjusted terms. As a result, aligned sales have strongly favored the PS4 & XBO (note that the third graph aligns the launches of the PS3 & 360):

But you'll notice that the bulk of the growth, the sharpest increases in the surpluses, have been in the holidays. The PS4 & XBO's combined surplus increased by more than 2.5 million units in the 2016 holiday period alone.

This is because sales have experienced a significant shift towards the holidays this generation thanks to official temporary Black Friday price cuts. While that trend began in 2011, it was solidified this generation. These big Black Friday deals deals have greatly diminished the effects of the permanent price cuts the systems have gotten. It has also resulted in consistently strong holiday sales, with combined PS4+XBO sales in Q4 far exceeding 5 million units for the past three years (and this year may make it a fourth). Compare this to combined PS2+Xbox sales, which only crossed the 5M mark in Q4 once (in 2002), and combined PS3+360 sales, which only did so twice (in 2010 & 2011).

The net effect of this is Gen 8 being more Q4-centric than ever, and total Q1-Q3 sales seeing far less variation than before. The Q1-Q3 period of 2015 saw combined PS4+XBO sales grow less than 3% YoY, while for the same periods in 2016 & 2017 were down about 5% each year. This year has seen Q1-Q3 sales grow something like 17% YoY, which is okay, but is only about 6% higher than Q1-Q3 2015. The biggest variations we've seen are in the holidays, with Q4 2015 being up 30% from Q4 2014 (though that was because Sony didn't offer any big discounts for the PS4 in the 2014 holiday season). Q4 2016 was down nearly 10% YoY, and Q4 2017 nearly matched Q4 2016 (though if you ignore October, the Nov.+Dec. period of 2017 was up about 4% YoY, not a huge difference but it's there).

The siphoning off of Q1-Q3 sales by Q4 (and esp. November) has also resulted in combined PS4+XBO sales in the non-holiday months just barely keeping pace with combined PS3+360 sales. This generation has looked big and healthy for conventional consoles compared to last gen, but you can thank Black Friday for that.

As for this year, the PS4's YoY growth can be attributed entirely to software. God of War, Spider-Man, and Red Dead all moved a good amount of hardware. But ignore April, September, and October, and we see baseline sales that have actually dipped ever so slightly. The Slim & Pro did help out a bit in 2017 (Q1-Q3 sales were up 17-18% YoY), but didn't produce a clear peak, and their upwards effect on sales has clearly ended. 2018 was the Year of the System Seller for the PS4 in the U.S.

As for the XBO, the One X has clearly helped out, with significant YoY improvements this year from a rather mediocre 2017. But again it hasn't produced a clear peak, and Q1-Q3 sales this year were weaker than those in 2015, and roughly flat with 2016. Also, September suggested that the One X effect might be coming to an end, with flat sales YoY for the month (October had Red Dead, which was also a system-seller for the XBO, so we can't make a determination).

The Pro and One X are unlikely to produce further sales growth unless Sony & MS introduce deep price cuts with the intent of having them fully supplant the slimline models. Q1 2019 will be the first big test for PS4 & XBO sales with current models at current prices. If we see both systems down noticeably, then that will likely signal them entering the terminal decline period of their lives. It's possible that deep cuts to the Pro and One X could drive some more sales growth, but with Gen 9 hardware known to be in the works and likely due for release in 2020, it's questionable if the Pro & One X will even get permanent price cuts of any kind. The Pro didn't even get a temporary cut for BF this year. And it's possible that such a cut might not result in any significant growth, as not everyone is likely to upgrade even at a reduced price. Eventually, no amount of attempts to stimulate sales will keep a system's sales from irreversibly declining.

In any case, the effects of the Pro and One X are overstated, and hardware revisions in general haven't had the effects they used to, just like how permanent price cuts haven't had the effects they used to. Without a breakdown between sales of the two, it's difficult to separate the effects of the Slim and Pro for the PS4, but between they two they failed to produce the kind of growth we saw with the PS3 Slim. The XBO S absolutely failed to produce significant growth past its first three months, and while the One X did help make Q1 this year the XBO's best Q1 to date and make Q2 its second-best Q2, it too was nothing like the 360 S in terms of what it did for sales.

Between the shift of a greater portion of annual sales to Q4 thanks to temporary BF price cuts and the relative failure of hardware revisions to produce strong growth, it's no wonder sales curves have been wonky this generation. But nevertheless the console cycle will continue unabated. The PS4 & XBO are at over 48M combined LTD, likely to be north of 53M by year's end. There is a maximum addressable market, with only so many households willing, able, and planning to buy a current-gen console at some point, and eventually Sony & MS will run out of potential customers to sell PS4s & XBOs to. The systems will enter the terminal decline phase of their lives before too long, regardless of their subversion of the usual "growth" and "peak" periods. By the end of 2011, the 360 & PS3 had a combined LTD total of 52.65M units, and in 2012 they began their declines. Since the PS4 & XBO will be at about that point by the end of this year, it wouldn't be a stretch to assume that they're likely going to start declining soon, probably next year, as the number of first-time buyers starts to dwindle. They'll probably end up at about the same ~70M units combined the PS3 & 360 ended up at, maybe slightly higher due to population growth potentially increasing the overall size of the addressable market as well as the potential for more mid-gen upgrades as usual since the Pro & One X were full spec upgrades (the first for home consoles since the Japan-only SuperGrafx) instead of just changes in form factor.

Well, that took longer and went on longer than I wanted, but I wanted to cover all my bases. Sorry if it sounded a bit ramble-y. Hope you all enjoyed the read and my attempts as sales analysis.