As already stated, don't look too often at the account. I am assuming you aren't a few years from retirement or anything like that. You are in this for the long haul. Some years you'll be down, but overall, you should see a 6% to 8% increase on average.Finally started regularly contributing to my Roth IRA before I can even think about it... I only bought FSMTX and FTIGX because I feel like that's the most straightforward option for someone who doesn't know much about this.

I've contributed for last year and this year, which feels good--however, it's been a few months now and I am unsure what type of growth I should be expecting. Looks like my account balance has just hovered around the same spot, even dropping slightly. I assume this is a 'put money in and forget about it' sort of account, but I just want to double check that what I'm doing is fine in the long run--buying FSTMX and FTIGX, specifically.

-

Ever wanted an RSS feed of all your favorite gaming news sites? Go check out our new Gaming Headlines feed! Read more about it here.

-

We have made minor adjustments to how the search bar works on ResetEra. You can read about the changes here.

Retirement-Era |OT| How to Invest For Retirement

- Thread starter TheTrinity

- Start date

- OT

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

OP

OP

Yeah, I'm sure you can find a decent CD. I don't know much about but there's plenty of references like this https://www.magnifymoney.com/blog/earning-interest/best-cd-rates967994263/

You have a pretty wide range of years there so I'm guessing it would be best to do repeating 2 year terms.

You have a pretty wide range of years there so I'm guessing it would be best to do repeating 2 year terms.

Did a quick calculation on a 4 percent rule calculator. Still on track to retire at 55 with enough to pay kid's college and leave a multi million dollar inheritance.

Just gotta keep hitting that modest savings increase each year!

Just gotta keep hitting that modest savings increase each year!

Good job!Did a quick calculation on a 4 percent rule calculator. Still on track to retire at 55 with enough to pay kid's college and leave a multi million dollar inheritance.

Just gotta keep hitting that modest savings increase each year!

Talk to me in 15 years

The geographic arbitrage helps a lot.

Did a quick calculation on a 4 percent rule calculator. Still on track to retire at 55 with enough to pay kid's college and leave a multi million dollar inheritance.

Just gotta keep hitting that modest savings increase each year!

Congratulations!

***First World Problem Alert***

I'm in a similar situation, but I honestly have no idea what I'd do if I retired. I don't hate my job/career so I'm not just going leave without something to retire to. I also don't have kids so leaving a legacy isn't something I'm interested in (although I could leave money to a charity). In the next 10 years or so I have a goal to find something I'd be passionate doing outside of work. Maybe volunteer or start a small business even if it doesn't have a huge upside.

edit - the 4% rule has a 30 year outlook so you might want to reduce your withdraw goal to something like 3.5% if you plan to retire at age 55.

Retiring to something is obviously very important!

And the 4% rule has plenty of margin in it. No need to over compensate with 3.5%, assuming you're somewhat flexible once you retire.

And the 4% rule has plenty of margin in it. No need to over compensate with 3.5%, assuming you're somewhat flexible once you retire.

And the 4% rule has plenty of margin in it. No need to over compensate with 3.5%, assuming you're somewhat flexible once you retire.

This is true and the withdrawal rule doesn't account for things like SS.

On the other hand, when you're older if you decide to "unretire" it can be difficult rejoin the work force with some professions. Withdrawal rates can depend on the persons situation, but 4% has failed when used over 30 year period despite being fairly conservative.

Agree with being flexible - therefore, if you're using 4% for a longer timeline it's a better idea if you're withdrawal provides 100k vs 30k because you can more easily adjust your spending if things get rough.

Last edited:

By the way, the Trinity Study (where the 4% rule comes from) was updated for 2018 with data through 2017. They also added failure rates up to 40 years and changed the analysis to use treasury bond rather than corporate bonds.

Cool, didn't know that they updated the Trinity Study. Thanks for sharing!By the way, the Trinity Study (where the 4% rule comes from) was updated for 2018 with data through 2017. They also added failure rates up to 40 years and changed the analysis to use treasury bond rather than corporate bonds.

Congratulations!

***First World Problem Alert***

I'm in a similar situation, but I honestly have no idea what I'd do if I retired. I don't hate my job/career so I'm not just going leave without something to retire to. I also don't have kids so leaving a legacy isn't something I'm interested in (although I could leave money to a charity). In the next 10 years or so I have a goal to find something I'd be passionate doing outside of work. Maybe volunteer or start a small business even if it doesn't have a huge upside.

edit - the 4% rule has a 30 year outlook so you might want to reduce your withdraw goal to something like 3.5% if you plan to retire at age 55.

Yeah, I'll most likely just semi-retire. I'll whittle my client base down to just a few, transition into meditation and adr for the games industry, and keep my side businesses/start new ones. I can never be truly idle. Just slow down and not "have" to work.

I went with a 3.5% withdrawal rate to be safe.

Being self employed helps as far as "re-entering" the workforce goes.This is true and the withdrawal rule doesn't account for things like SS.

On the other hand, when you're older if you decide to "unretire" it can be difficult rejoin the work force with some professions. Withdrawal rates can depend on the persons situation, but 4% has failed when used over 30 year period despite being fairly conservative.

Agree with being flexible - therefore, if you're using 4% for a longer timeline it's a better idea if you're withdrawal provides 100k vs 30k because you can more easily adjust your spending if things get rough.

I apologize if this is the wrong place to post this, but I am unsure of where else would be best.

I was covered under a HDHP with my previous employer which included an HSA. The HSA custodian is now charging $5 monthly fees. I am not enrolled in a HDHP with my new employer. Am I allowed to open an HSA with another custodian just so I can rollover these funds to avoid fees? I will not make any contributions whatsoever as I know I am not allowed to do so without being covered by a HDHP. Am I still allowed to do this if I am not covered by a HDHP?

Thanks guys!

I was covered under a HDHP with my previous employer which included an HSA. The HSA custodian is now charging $5 monthly fees. I am not enrolled in a HDHP with my new employer. Am I allowed to open an HSA with another custodian just so I can rollover these funds to avoid fees? I will not make any contributions whatsoever as I know I am not allowed to do so without being covered by a HDHP. Am I still allowed to do this if I am not covered by a HDHP?

Thanks guys!

Ally Bank CDs are in the 2 to 2.6% range for 12 month to 5 year terms.

Yeah, I'm sure you can find a decent CD. I don't know much about but there's plenty of references like this https://www.magnifymoney.com/blog/earning-interest/best-cd-rates967994263/

You have a pretty wide range of years there so I'm guessing it would be best to do repeating 2 year terms.

Thank you both! I thought CD rates had really tanked, but I would be OK with anything that can keep me near inflation at least, which a 2-3% range should roughly muster. Really appreciated, thanks again.

I apologize if this is the wrong place to post this, but I am unsure of where else would be best.

I was covered under a HDHP with my previous employer which included an HSA. The HSA custodian is now charging $5 monthly fees. I am not enrolled in a HDHP with my new employer. Am I allowed to open an HSA with another custodian just so I can rollover these funds to avoid fees? I will not make any contributions whatsoever as I know I am not allowed to do so without being covered by a HDHP. Am I still allowed to do this if I am not covered by a HDHP?

Thanks guys!

If you call your current HSA custodian and ask them to do a direct transfer of the funds to the new custodian it doesn't count as a rollover and does not need to be reported on your taxes at all.

As for your actual question about whether rollovers are disallowed, I don't think so, but I'm not a lawyer.

If you call your current HSA custodian and ask them to do a direct transfer of the funds to the new custodian it doesn't count as a rollover and does not need to be reported on your taxes at all.

As for your actual question about whether rollovers are disallowed, I don't think so, but I'm not a lawyer.

Thanks! I am just going to do a direct transfer rather than a rollover. Seems much easier.

Hey guys, started a new job and need some help with investing.

It's a large company so they have their own investment plans going on, it's not through Fidelity or Vanguard, etc. I put 100% into US large company index which is basically the S&P 500 index fund. They don't have any bond choices from what I can see. The only other index funds I can see are US Small/Mid company index and Foreign all company index funds. According to the company I should not put 100% in just the fund I have now, but they have the best fee of .01%.

Anyway I'm looking for advice on how I should break it down. I'm 30 years old and probably won't retire until I'm in my 60s. I prefer to be hands off and generally risk free, I just want it to grow slow and steady.

It's a large company so they have their own investment plans going on, it's not through Fidelity or Vanguard, etc. I put 100% into US large company index which is basically the S&P 500 index fund. They don't have any bond choices from what I can see. The only other index funds I can see are US Small/Mid company index and Foreign all company index funds. According to the company I should not put 100% in just the fund I have now, but they have the best fee of .01%.

Anyway I'm looking for advice on how I should break it down. I'm 30 years old and probably won't retire until I'm in my 60s. I prefer to be hands off and generally risk free, I just want it to grow slow and steady.

OP

OP

Seems good enough to me. Maybe split it like 75/20/5 among Large/Mid/Small indexes if you feel like it.

So I asked a few months ago about my Rollover IRA and I finally started investing the money that was in there from my old job. My question is do I have to open a traditional IRA account or can I continue to use the Rollover IRA account to make future purchases? Is the account still tax deferred as I invest? Lastly, since I am now purchasing funds with that money, will I have to report it to the IRS? I don't think I made a report years ago when my old company went under and rolled over my 401K to the Rollover IRA. Thanks.

Also another question about my portfolio. Im in the military and switched to the new Blended Retirement System that matches up to 5%. I know its suggested to max out an ira after meeting the % max of the 401k, but would it be worth it if Im in TSP? Seems the reason for maxing an iRA is the expenses, but TSP is one of the lowest already at I think .033. My plan was to keep putting money into TSP and then rolling over to my fidelity account when I get out.

I just got a new job and because of transisiton a double salary, and can finally afford to start looking at this thread for real. Just started saving at 25 years old. Not much, but I put around a €1000 into two medium risk stocks and put €2500 into a savings account for home ownership - it's called BSU in Norway, don't know if it exists in other countries, basically you are allowed to save 25 000 NOK a year and if you do you get a guaranteed 5 000 (25%) divident through tax returns. The catch is the money must be used to purchase a living space and you are only allowed to save until you are 33 years old. I also started to save €20 per month into a low risk retirement fund. Not a great sum, but you have to start somewhere.

Now all I need is motivation to continue putting money into the market when I don't get double paid :D

Now all I need is motivation to continue putting money into the market when I don't get double paid :D

OP

OP

I just got a new job and because of transisiton a double salary, and can finally afford to start looking at this thread for real. Just started saving at 25 years old. Not much, but I put around a €1000 into two medium risk stocks and put €2500 into a savings account for home ownership - it's called BSU in Norway, don't know if it exists in other countries, basically you are allowed to save 25 000 NOK a year and if you do you get a guaranteed 5 000 (25%) divident through tax returns. The catch is the money must be used to purchase a living space and you are only allowed to save until you are 33 years old. I also started to save €20 per month into a low risk retirement fund. Not a great sum, but you have to start somewhere.

Now all I need is motivation to continue putting money into the market when I don't get double paid :D

When you say two medium risk stocks, do you mean individual stocks? Just because this is not something that would be recommended here. That home savings plan sounds pretty cool though.

Anyone know of a good financial investment company that offers daily/weekly investing ideas for a monthly price?

This sounds like a really awful idea. You want to pay someone to tell you a new thing to buy every day? That's certainly not a winning strategy for Retirement-Era. You may be looking for the day-trading/stock picking thread. I recommend reading the OP to see what we're about here.

I have about $20,000 right now in my IRA that my company opened and I have some investments in Apple, Microsoft, Disney (all 3 because I like these companies) and then I have some funds in VGT and FBGRX, blue chip funds.

Any recommendations on how to diversify a little more for my portfolio? I have $5k to work with here.

Any recommendations on how to diversify a little more for my portfolio? I have $5k to work with here.

Yes, individual stocks. I'm working my way up to a nice portfolio, with tips from my father. He has spent his whole life in stock trading but I have never had my own money to consider learning.When you say two medium risk stocks, do you mean individual stocks? Just because this is not something that would be recommended here.

Also another question about my portfolio. Im in the military and switched to the new Blended Retirement System that matches up to 5%. I know its suggested to max out an ira after meeting the % max of the 401k, but would it be worth it if Im in TSP? Seems the reason for maxing an iRA is the expenses, but TSP is one of the lowest already at I think .033. My plan was to keep putting money into TSP and then rolling over to my fidelity account when I get out.

TSP is basically the lowest fees out there. I'd max out the TSP as long as your happy with the choices in the plan

I am after i did some research. Seems c fund is basically the s&p500 and i fund is international. Also word is that i fund will be getting emerging markets added next year.

I'm sorry I still don't understand Roth IRA

When I put money in it is somebody automatically doing whatever the investment is for me for this magical compound interest? Or do I have to do something?

No, after you setup an account you can direct the funds to basically whatever you want. It's easy to setup a Roth account online with a company like Vanguard (that's who I use). After you setup the account buy one of their funds. Vanguard Total Stock ETF (VTI) is a good place to start. Their target retirement funds are also a good choice. Once you build a sizable portfolio (401k, taxable, roth, etc) of about 50k consider implementing a 3 fund portfoliofor additional diversification.

Last edited:

This is not the thread you are looking for.So I'm looking to get serious about budgeting/saving/investing. Is this thread just about retirement savings or do you also discuss shorter term investing/saving?

Try here: https://www.resetera.com/threads/in...ividends-no-tales-from-the-crypto-here.28604/

Everybody notice mortgage rates have gone from ~3.8% to ~4.75 over the past year, and a quarter percent over the past couple months?

Everybody notice mortgage rates have gone from ~3.8% to ~4.75 over the past year, and a quarter percent over the past couple months?

The federal reserve has raised the prime interest rate to counter inflation fears. This has a direct effect on the overall mortgage market.

The federal reserve has raised the prime interest rate to counter inflation fears. This has a direct effect on the overall mortgage market.

Right. Just noting as someone who just bought a house (idea being to have it paid off before retirement) that the lack of robust available inventory (at least here in KC metro) is/was sending prices soaring. I'm watching it with my own eyes. Rates going up (vis a vis the fed) may help cool that off. I don't think it will though, not until they're in the 6s or 7s.

I'm sorry I still don't understand Roth IRA

When I put money in it is somebody automatically doing whatever the investment is for me for this magical compound interest? Or do I have to do something?

An IRA is basically a holding account where your money sits. Once your money is transferred from your bank account to your IRA, you can then go check out different funds and buy those funds. Compound starts once you buy a share of a fund.

A ROTH IRA is basically an account which you are taxed upfront. An IRA, or traditional IRA, is basically taxed withheld till you retire, where you are than taxed.

No, after you setup an account you can direct the funds to basically whatever you want. It's easy to setup a Roth account online with a company like Vanguard (that's who I use). After you setup the account buy one of their funds. Vanguard Total Stock ETF (VTI) is a good place to start. Their target retirement funds are also a good choice. Once you build a sizable portfolio (401k, taxable, roth, etc) of about 50k consider implementing a 3 fund portfoliofor additional diversification.

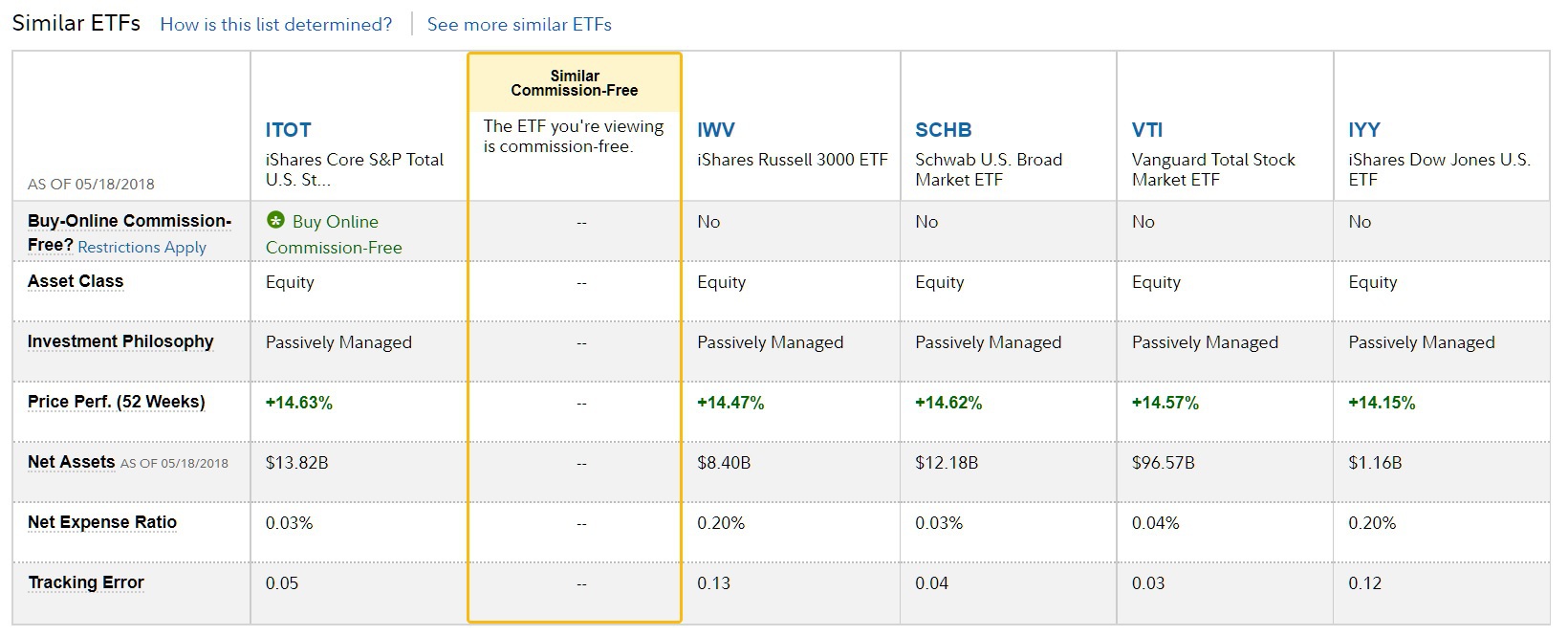

Yea, I basically have the equivalent to VTI with Fidelity. My fund is the ITOT, which is the equivalent to VTI.

The funds you choose are based on you, your age, and your risk tolarance. No one should be telling you which fund to go with because everyone is different. I suggest reading the op. Maybe check YouTube videos and google search for terms like retirement portolio, mutual funds, etf, expense ratio, index funds, bonds, etc..

As to losing money, you definitely can lose money. But if you invest and hold till you retire, the loses over the course of 30-40 years are negligible. You only really lose money if u you take out your money.

Google a chart of the s&p500 over its life and you can see, even with crashes, the market has continued to rise.

I recently transferred/reallocated my 401k from BlackRock LifePath Index 2050 LIPKX to Fidelity 500 Index Premium FUSVX. The reason was that the FUSVX was cheaper expense ratio as well as it's unlikely I will stay at current employer and will probably end up rolling over my 401k into future employer's plan. What do some of you veterans have to say? Good or bad move? It probably won't matter that much if I leave next year, but there is possibility I could be here another three years if I get a promotion in 6 months.

It's nice to see a thread like this doing well here. I was worried for a while that it was going to get buried in favor of crypto threads.

I hate crypto. It's ruining the PC builder market.It's nice to see a thread like this doing well here. I was worried for a while that it was going to get buried in favor of crypto threads.

If by "ruining" you mean "boosting demand for products in an industry which has been stagnant or declining for decades" then yes, I agree with you. Crypto is basically saving the PC market at this point by giving people actual reasons to build PC's above and beyond the small niche that is PC gaming. For investors who have been paying attention, buying shares of any company who sells products to crypto miners has been immensely profitable (e.g. NVDA, AMD, MU, INTC, etc.)

PC's in general have been declining, not PC Building. PC Building has grown with the rise of Steam, Youtube, and Twitch.If by "ruining" you mean "boosting demand for products in an industry which has been stagnant or declining for decades" then yes, I agree with you. Crypto is basically saving the PC market at this point by giving people actual reasons to build PC's above and beyond the small niche that is PC gaming.

Those things are all related to PC gamingPC's in general have been declining, not PC Building. PC Building has grown with the rise of Steam, Youtube, and Twitch.

Hi, guys!

So, I'm 30 years old and don't have any money in retirement. I NEED to start. It is something I have been thinking about for a while now. The only thing is, I feel extremely overwhelmed by all the information available - and confused.

Currently, my job offers a 401k plan, but does not match at all, so investing in that from what I've read is pretty much pointless.

I've been doing some reading here and other places, and it looks my best bet is to invest in a ROTH IRA. I make 42k a year and within the next 5 years I hope to be nearly doubling that. The thing is, I don't have much money in my savings, about 2000~. This is money I would like to move to a retirement plan by the end of the year. Also, my goal starting next month when my health insurance rate at work changes is to invest about $120 into retirement each month starting next month?? (Not sure if this is possible without having a lump sum to start with?)And then by the end of the year around $300, when I have a loan paid off.

My questions are,

1) Is there anyway for me to open a Roth IRA account within the next month with only putting about 120~ into it each month? And then at the end of the year putting a larger lump sum in and increasing the monthly total I add at the end of the year. Or would it be wiser to just wait until the end of the year when I will be able to put more in? Are there fees/taxes/etc for starting with a small amount?

2) Are there any good YouTube channels for people just starting out?

3) Once I get some decent amount of money established in my Roth IRA account (ie, 5 years from now) when and how can I decide if I want to start investing it in stocks/bonds/etc?

I'm sorry if these questions have been ask ad nausium. These are just my own personal questions I have and ones that I have the most right now.

I greatly appreciate any information anyone is able to provide. I will be reading this thread more throughly over the coming weeks/months and hopefully years!

So, I'm 30 years old and don't have any money in retirement. I NEED to start. It is something I have been thinking about for a while now. The only thing is, I feel extremely overwhelmed by all the information available - and confused.

Currently, my job offers a 401k plan, but does not match at all, so investing in that from what I've read is pretty much pointless.

I've been doing some reading here and other places, and it looks my best bet is to invest in a ROTH IRA. I make 42k a year and within the next 5 years I hope to be nearly doubling that. The thing is, I don't have much money in my savings, about 2000~. This is money I would like to move to a retirement plan by the end of the year. Also, my goal starting next month when my health insurance rate at work changes is to invest about $120 into retirement each month starting next month?? (Not sure if this is possible without having a lump sum to start with?)And then by the end of the year around $300, when I have a loan paid off.

My questions are,

1) Is there anyway for me to open a Roth IRA account within the next month with only putting about 120~ into it each month? And then at the end of the year putting a larger lump sum in and increasing the monthly total I add at the end of the year. Or would it be wiser to just wait until the end of the year when I will be able to put more in? Are there fees/taxes/etc for starting with a small amount?

2) Are there any good YouTube channels for people just starting out?

3) Once I get some decent amount of money established in my Roth IRA account (ie, 5 years from now) when and how can I decide if I want to start investing it in stocks/bonds/etc?

I'm sorry if these questions have been ask ad nausium. These are just my own personal questions I have and ones that I have the most right now.

I greatly appreciate any information anyone is able to provide. I will be reading this thread more throughly over the coming weeks/months and hopefully years!

Exactly, which is mostly the people who build their own PC's.

Hi, guys!

So, I'm 30 years old and don't have any money in retirement. I NEED to start. It is something I have been thinking about for a while now. The only thing is, I feel extremely overwhelmed by all the information available - and confused.

Currently, my job offers a 401k plan, but does not match at all, so investing in that from what I've read is pretty much pointless.

I've been doing some reading here and other places, and it looks my best bet is to invest in a ROTH IRA. I make 42k a year and within the next 5 years I hope to be nearly doubling that. The thing is, I don't have much money in my savings, about 2000~. This is money I would like to move to a retirement plan by the end of the year. Also, my goal starting next month when my health insurance rate at work changes is to invest about $120 into retirement each month starting next month?? (Not sure if this is possible without having a lump sum to start with?)And then by the end of the year around $300, when I have a loan paid off.

My questions are,

1) Is there anyway for me to open a Roth IRA account within the next month with only putting about 120~ into it each month? And then at the end of the year putting a larger lump sum in and increasing the monthly total I add at the end of the year. Or would it be wiser to just wait until the end of the year when I will be able to put more in? Are there fees/taxes/etc for starting with a small amount?

2) Are there any good YouTube channels for people just starting out?

3) Once I get some decent amount of money established in my Roth IRA account (ie, 5 years from now) when and how can I decide if I want to start investing it in stocks/bonds/etc?

I'm sorry if these questions have been ask ad nausium. These are just my own personal questions I have and ones that I have the most right now.

I greatly appreciate any information anyone is able to provide. I will be reading this thread more throughly over the coming weeks/months and hopefully years!

1. I'm pretty sure you can open with $0 if you want. An IRA is just an account where your money is going to. Think of it as a wallet where you will put money in, use that money to buy funds, send money to if you sell funds, and where you will send money out. Investing doesn't start until you buy your first fund or stock.

2. Vanguard, Morningstar, Jack Bogle, Fidelity. Just search for investing for retirement. Also check out bogleheads.org and even reddit.

3. Google different styles of retirement portfolios. The one that everyone talks about is a 3 fund portfolio(US index, international index, bonds) but there are a lot more than that.

Just know that some funds do have a minimum amount to buy in. For me, since I don't have enough yet to get into a mutual fund(min is $2500 with Fidelity) I got into ETF's, which cost the price of the fund. For example, I bought shares of ITOT, which is an S&P500 fund with Blackrock. To buy into that fund I had to buy a share, which cost me ~$60.

Also read up on the differences between a mutual fund and an ETF. AND make sure you read up and watch some videos on compounding interest. You may change your mind about waiting 5 years to build money to invest after seeing what happens if you hold off on investing. Check out some compound interest calculators and see what that 5 year difference will cost you in 30-40 years.

Last edited:

Guys I'm so dumb.

So let's say I open an account with, whatever, Vanguard. I do the target retirement fund. That is my Roth IRA? Right? And I don't have to actively pay attention to it? What happens if five years from now I finally know what I'm doing - can I move the money out of the target retirement fund?

So let's say I open an account with, whatever, Vanguard. I do the target retirement fund. That is my Roth IRA? Right? And I don't have to actively pay attention to it? What happens if five years from now I finally know what I'm doing - can I move the money out of the target retirement fund?

An IRA is an account for retirement. A Roth is a type of IRA account. Inside your IRA, you can search for funds which you will invest in. A target fund is a type of mutual fund that basically does the allocation of stocks to bonds for you. Say you buy into a 2050 fund. The allocation will start with a heavy allocation to the market vs the bond. As you get closer to your target date of 2050, the fund will automatically start going more towards bonds vs stocks. Doing so reduces the risk of any catastrophic crash as you near retirement. As you said, it's a set it and forget it fund. If sometime later you decide you want to be more hands on, you can sell the 2050 fund and use the money from selling to buy another fund.

Here are a couple potentially dumb questions...

I want to set up a Roth IRA and 529 in tandem for my daughter's college fund. It seems like a decent way to cover my bases in case she either doesn't want to go to college or ends up in another state for some reason, financial aid relief, investment options/flexibility, etc.

So my questions:

1. Is this a dumb idea?

2. How do they know you're using withdrawn IRA funds to pay for college? I would assume you indicate it in your taxes?

3. Is there a possibility this rule could change in the future for Roth IRAs? I only learned recently that you can withdraw from it without penalty for higher education. Is that something that could ever change? Or would I be grandfathered in anyway even if it did?

I want to set up a Roth IRA and 529 in tandem for my daughter's college fund. It seems like a decent way to cover my bases in case she either doesn't want to go to college or ends up in another state for some reason, financial aid relief, investment options/flexibility, etc.

So my questions:

1. Is this a dumb idea?

2. How do they know you're using withdrawn IRA funds to pay for college? I would assume you indicate it in your taxes?

3. Is there a possibility this rule could change in the future for Roth IRAs? I only learned recently that you can withdraw from it without penalty for higher education. Is that something that could ever change? Or would I be grandfathered in anyway even if it did?

I'm not sure where to go with my savings anymore. My employer doesn't offer a 401k so I don't have that. Instead I have 30k in a VFIAX index fund through Vanguard. I've had it for over a year and a half now. The growth has been pretty good, at about 13%. Should I continue reinvesting my earnings in this fund? I've had that option since the account's inception, to redistribute any gains back into the fund. Or should I target a different fund and invest elsewhere?

This is the only type of savings I really have, besides 3k in emergency funds in a regular checking account.

This is the only type of savings I really have, besides 3k in emergency funds in a regular checking account.

I know this isn't directly on point, but does anyone here use Mint? I have a good handle on my finances, but it's still pretty broad strokes, as in I only approximately know what percentage of my salary is going to what annually.

But I feel kind of skeeved about giving Mint access to all of my financial accounts. And I might be too lazy for an Excel spreadsheet :P

But I feel kind of skeeved about giving Mint access to all of my financial accounts. And I might be too lazy for an Excel spreadsheet :P